Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

How Much Do You Really Need to Buy a Home?

From 0% down VA and USDA options to 3% conventional and 3.5% FHA loans, here’s what Virginia buyers should know about real down payment requirements and smart trade-offs.

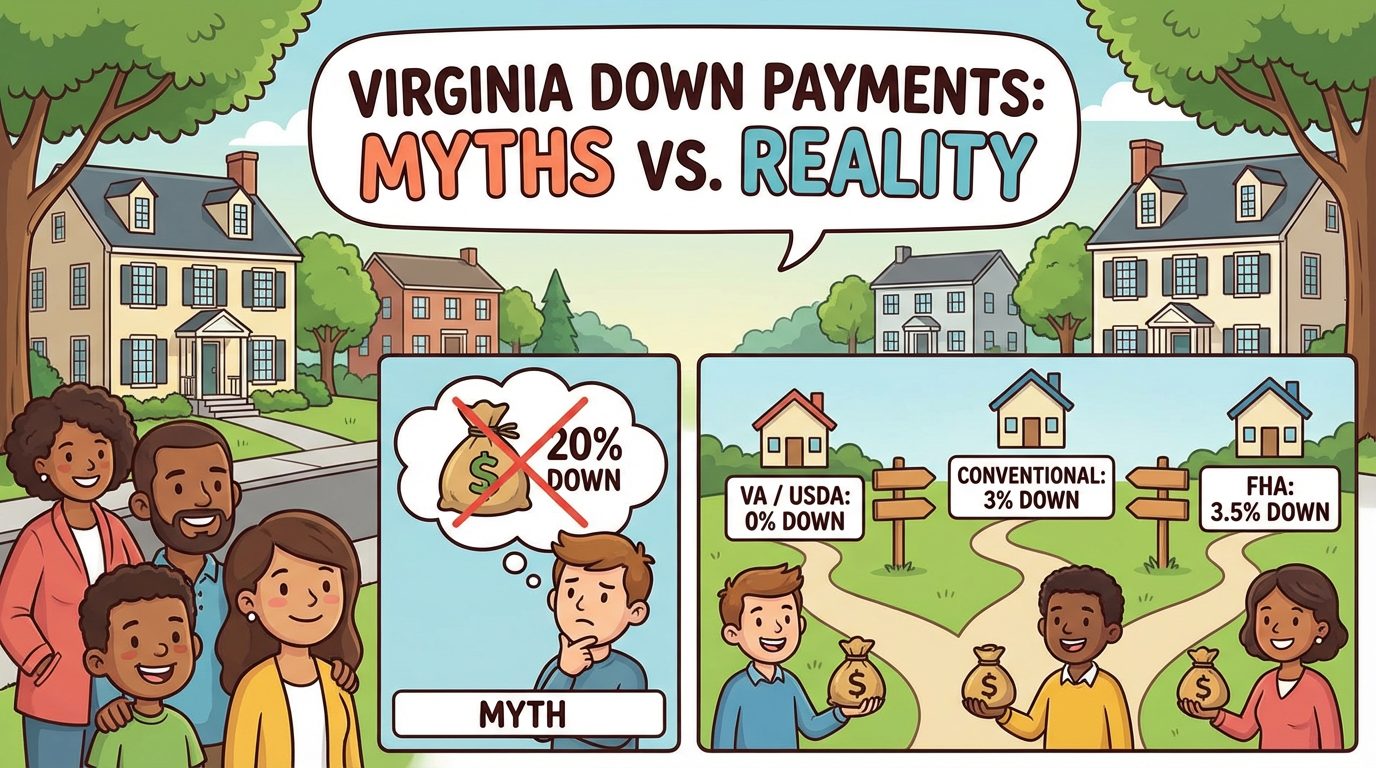

The Biggest Virginia Down Payment Myth: “You Need 20% Down.”

One of the most common homebuying myths is that you must put 20% down to purchase a home. In reality, many Virginia buyers purchase with far less. While 20% can be beneficial in certain cases, it’s not a universal requirement, and waiting years to save that amount can unnecessarily delay homeownership.

Common Down Payment Options for Virginia Homebuyers

Virginia homebuyers often use low-down-payment options, especially first-time buyers and those prioritizing savings for moving costs, repairs, or an emergency fund.

Typical down payment ranges you’ll commonly see in Virginia:

– 3–5% down: a frequent range for many buyers using popular loan programs

– 0% down: available through specific government-backed programs for eligible borrowers

0% Down Loans in Virginia: VA and USDA

Some loan programs allow qualified buyers to purchase a home with no down payment at all.

VA Loans (0% down)

VA loans are designed for eligible service members, veterans, and some surviving spouses. If you qualify, this can be one of the most powerful ways to buy a home in Virginia with minimal upfront cash.

USDA Loans (0% down)

USDA loans are intended for eligible buyers purchasing in qualifying rural and some suburban areas. In Virginia, this can apply to many communities outside dense city centers, depending on property location and program rules.

Low Down Payment “Staples” in Virginia: FHA and Conventional

If 0% down isn’t a fit, many Virginia buyers still have options well below 20%.

FHA Loans (3.5% down)

FHA loans require 3.5% down for borrowers who meet credit guidelines, including a commonly referenced minimum credit score of 580 or higher for the 3.5% down option. This program is often used by buyers who want flexible qualifying standards.

Conventional Loans (as low as 3% down)

Some conventional programs permit as little as 3% down. These programs can be a strong fit for buyers with solid credit and stable income who want a low down payment without using an FHA loan.

The Real Trade-Offs: What a Bigger Down Payment Can Do

Even though you don’t always need 20% down, a larger down payment can still provide meaningful benefits.

A higher down payment may:

– Lower your monthly mortgage payment by reducing the loan amount

– Help you avoid mortgage insurance in some scenarios (especially when reaching the typical 20% equity threshold)

That said, putting more down isn’t automatically “better” if it drains savings. A smart plan balances monthly affordability with keeping enough cash available for closing costs, moving expenses, and home maintenance.

First-Time Homebuyer Help in Virginia: Reducing Upfront Cash Pressure

Many first-time buyer programs are designed to reduce the cash needed upfront. Depending on the program, support may help with down payment and/or other early homeownership costs, making it easier to buy sooner rather than later.

If you’re buying your first home in Virginia, whether in Northern Virginia, Richmond, Virginia Beach, Chesapeake, or smaller communities across the Commonwealth, these programs can be a practical way to move from “almost ready” to “ready.”

A Smarter Way to Think About Your Virginia Down Payment

The idea that you must save 20% down to buy a home is one of the most persistent myths in real estate. In Virginia, many buyers use 3–5% down, and some qualified borrowers can even buy with 0% down using VA or USDA loans. Options like FHA (3.5% down with qualifying credit) and select conventional programs (3% down) can make homeownership more accessible, while a larger down payment can still reduce monthly costs and potentially help you avoid mortgage insurance. The best down payment strategy is the one that fits your eligibility, your monthly budget, and your need to keep cash on hand after closing.

People Also Ask

Q: Do I need 20% down to buy a home in Virginia?

A: No. Many Virginia buyers put 3–5% down, and some programs allow 0% down for eligible borrowers.

Q: What is the minimum down payment for an FHA loan in Virginia?

A: FHA loans typically require 3.5% down if the borrower meets credit criteria, commonly including a credit score of at least 580 for the 3.5% down option.

Q: Can I buy a home in Virginia with no down payment?

A: Yes, if you qualify. VA loans can offer 0% down for eligible military-connected borrowers, and USDA loans can offer 0% down for eligible buyers purchasing in qualifying areas.

Q: Is 3% down possible with a conventional mortgage?

A: Yes. Some conventional loan programs permit 3% down, depending on eligibility and lender guidelines.

Q: What are the benefits of putting more money down on a house?

A: A higher down payment can lower your monthly payment and may help you avoid mortgage insurance, depending on the loan type and your equity level.

Q: Are there programs to help first-time homebuyers in Virginia?

A: Yes. First-time buyer programs can help reduce the upfront cash needed, which can make it easier to afford the initial costs of buying a home.